In today’s fast-moving business environment, tax is no longer just a once-a-year obligation—it’s a strategic opportunity. Businesses and individuals who treat tax planning as a proactive process, rather than a last-minute task, often unlock significant savings and stronger financial control.

At its core, effective tax planning is about legally minimizing your tax liability while aligning with your financial goals. Done right, it doesn’t just reduce your tax bill—it improves cash flow, supports growth, and enhances long-term stability.

Why Tax Planning Matters More Than Ever

With evolving regulations, digital compliance systems, and increasing scrutiny from tax authorities, reactive tax filing is no longer enough. Modern businesses need a forward-looking approach that anticipates liabilities and identifies opportunities before deadlines arrive.

Effective tax planning allows you to:

Retain more of your earnings

Avoid penalties and compliance risks

Improve financial forecasting

Make smarter investment decisions

Key Strategies to Reduce Your Tax Bill

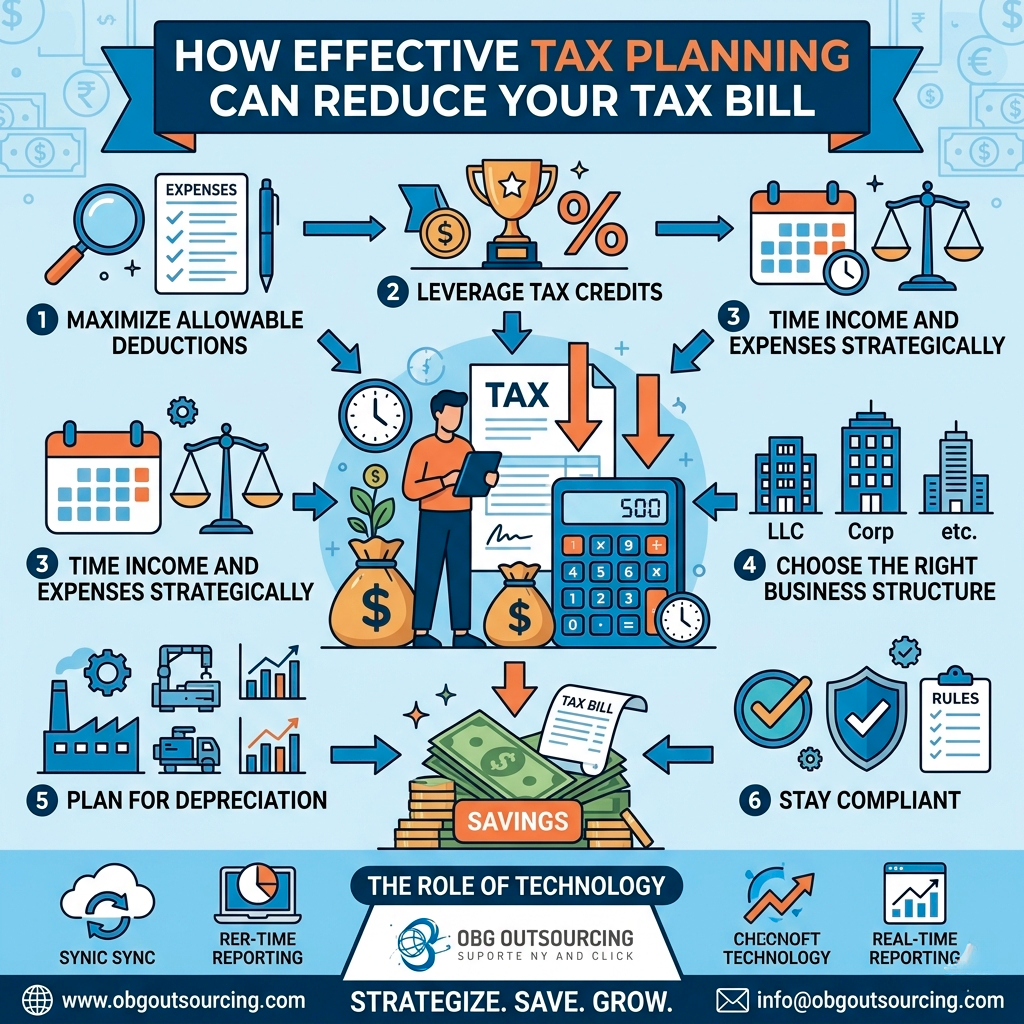

1. Maximize Allowable Deductions

Many businesses miss out on deductions simply due to lack of awareness or poor record-keeping. Expenses such as operational costs, employee benefits, depreciation, and professional fees can significantly lower taxable income when properly documented.

2. Leverage Tax Credits

Unlike deductions, tax credits directly reduce the amount of tax you owe. Identifying applicable credits—whether for investments, exports, innovation, or sustainability—can result in substantial savings.

3. Time Your Income and Expenses Strategically

Timing plays a critical role in tax planning. Deferring income or accelerating expenses (where legally permitted) can shift tax liabilities to more favorable periods, improving short-term cash flow.

4. Choose the Right Business Structure

Your entity type impacts how you are taxed. Whether operating as a sole proprietor, partnership, or corporation, the structure should align with your revenue model and long-term plans to optimize tax efficiency.

5. Plan for Depreciation and Capital Investments

Investing in assets such as equipment or technology can offer depreciation benefits over time. Strategic planning ensures you maximize these advantages without disrupting your cash reserves.

6. Stay Compliant with Changing Regulations

Tax laws are constantly evolving. Staying updated ensures you take advantage of new benefits while avoiding costly penalties due to non-compliance.

The Role of Technology in Modern Tax Planning

Digital tools and cloud accounting systems have transformed tax management. Real-time tracking, automated reporting, and data analytics allow businesses to monitor their tax position throughout the year—not just at filing time.

This shift enables:

Faster decision-making

Greater accuracy

Reduced manual errors

- Better audit readiness

Common Mistakes to Avoid

Even well-intentioned businesses can fall into these traps:

Waiting until year-end to plan taxes

Mixing personal and business finances

Ignoring documentation and record-keeping

Overlooking small but cumulative deductions

Relying solely on outdated tax strategies

Avoiding these mistakes can make a measurable difference in your final tax liability.

A Smarter Approach to Tax Efficiency

Effective tax planning is not about aggressive tactics—it’s about informed, strategic decisions made consistently throughout the year. Businesses that adopt this mindset gain a competitive edge by preserving capital and reinvesting it into growth.

At OBG Outsourcing, we believe tax planning should be simple, transparent, and aligned with your business goals. With the right guidance, reducing your tax bill becomes less about stress—and more about strategy.

_(6).jpg)

1.png)

_(5).jpg)

.jpg)

_(4).jpg)

_(1).jpg)

_(2).jpg)

.png)