Filing taxes isn’t just a once-a-year task—it’s a critical financial process that can shape your business stability and personal financial health. Yet, even experienced professionals and growing businesses often fall into avoidable traps. These mistakes don’t just cost money; they can trigger audits, penalties, and unnecessary stress.

Let’s break down the most common tax filing mistakes—and more importantly, how to avoid them with confidence.

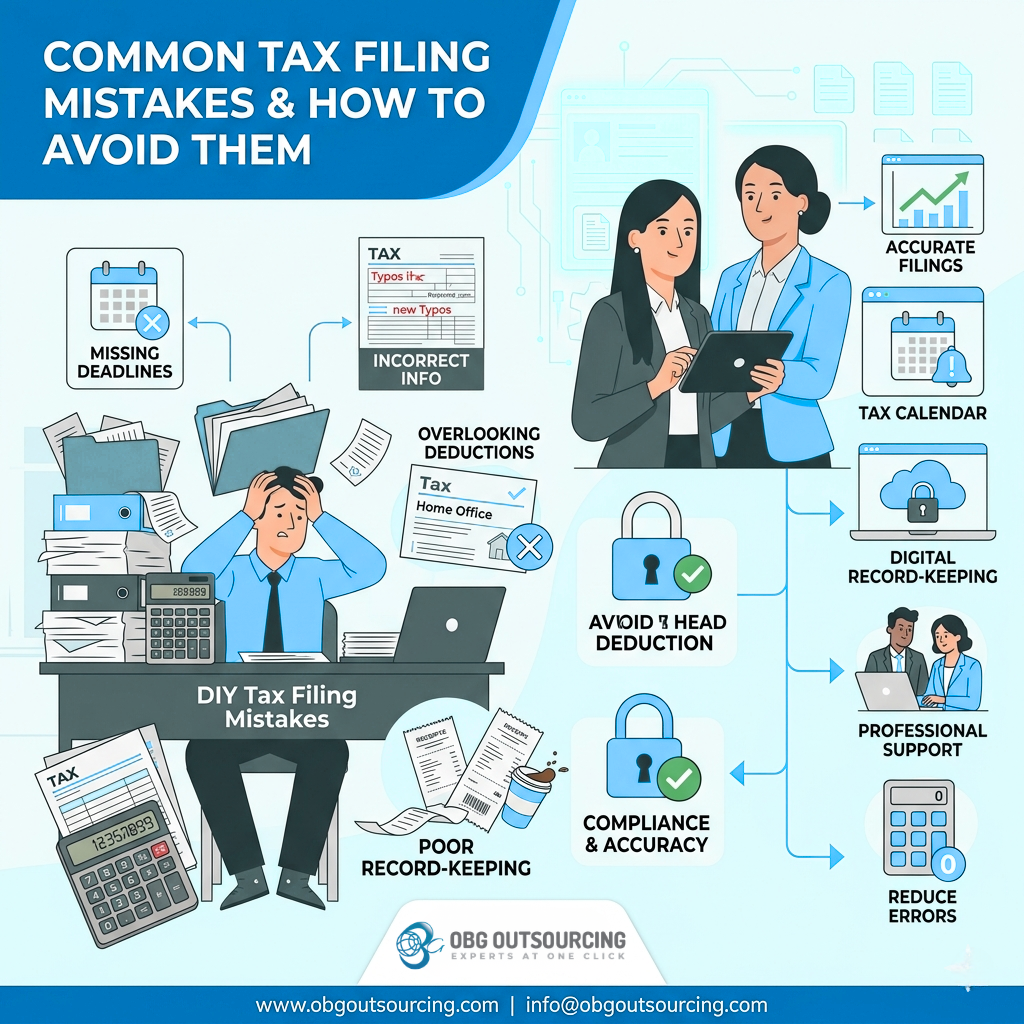

1. Missing Deadlines (and Underestimating Them)

Deadlines seem obvious, but they’re one of the most frequently missed aspects of tax filing. Whether it’s due to poor planning or last-minute scrambling, late submissions can result in penalties and interest.

How to avoid it:

Create a tax calendar that includes all key filing dates—not just annual returns but also quarterly filings, estimated taxes, and compliance deadlines. Better yet, automate reminders or work with a tax partner who tracks deadlines for you.

2. Incorrect or Incomplete Information

A small typo in your Social Security Number, business ID, or bank details can delay processing—or worse, invalidate your return.

How to avoid it:

Double-check all entries before submission. Use digital tools or professional services that validate information in real time. Accuracy is not optional—it’s essential.

3. Overlooking Eligible Deductions

Many taxpayers either miss deductions entirely or underestimate what they can claim. This leads to overpaying taxes unnecessarily.

How to avoid it:

Stay informed about deduction categories relevant to your situation—whether it’s business expenses, home office use, or depreciation. Keeping organized records throughout the year makes claiming deductions easier and more accurate.

4. Misclassifying Employees and Contractors

This is a critical issue for businesses. Misclassification can lead to compliance issues, fines, and even legal complications.

How to avoid it:

Understand the distinction between employees and independent contractors based on control, work structure, and payment methods. When in doubt, consult a tax expert to ensure proper classification.

5. Ignoring Changes in Tax Laws

Tax regulations evolve frequently. Relying on outdated knowledge can lead to errors or missed opportunities.

How to avoid it:

Stay updated with the latest tax reforms and compliance requirements. Subscribing to financial updates or partnering with a knowledgeable outsourcing firm can keep you ahead of changes.

6. Poor Record-Keeping

Disorganized financial records make tax filing harder, increase the risk of errors, and complicate audits.

How to avoid it:

Maintain a consistent record-keeping system—digitize receipts, track expenses in real time, and store documents securely. Clean records are your best defense during audits.

7. Math Errors and Manual Calculations

Manual calculations increase the likelihood of mistakes, especially when dealing with complex financial data.

How to avoid it:

Use reliable accounting software or automated tax tools to handle calculations. Technology minimizes human error and speeds up the filing process.

8. Filing Under the Wrong Status

Choosing the wrong filing status can impact your tax liability significantly.

How to avoid it:

Review your eligibility for different filing statuses each year. Changes in marital status, dependents, or business structure can alter your ideal category.

9. Not Reporting All Income Sources

Freelance work, side gigs, investments—every income stream counts. Failing to report them can trigger audits.

How to avoid it:

Track all income sources throughout the year and reconcile them before filing. Transparency is key to staying compliant.

10. Trying to Do Everything Alone

While DIY tax filing might seem cost-effective, it often leads to overlooked details and costly errors.

How to avoid it:

Consider outsourcing your tax preparation to experts who understand compliance, deductions, and strategy. It’s not just about filing—it’s about optimizing your financial outcomes.

Why Smart Businesses Choose Outsourcing

Modern businesses are moving beyond traditional methods and embracing smarter solutions. Partnering with a trusted provider like OBG Outsourcing allows you to:

Reduce errors and ensure compliance

Save time and internal resources

Gain expert insights into tax optimization

Stay updated with changing regulations

Outsourcing transforms tax filing from a stressful obligation into a streamlined, strategic process.

Final Thoughts

Tax filing doesn’t have to be overwhelming—or risky. Most mistakes stem from lack of preparation, outdated knowledge, or simple oversight. By adopting proactive strategies and leveraging expert support, you can avoid these pitfalls entirely.

In today’s fast-paced financial landscape, accuracy isn’t just important—it’s your competitive advantage.

_(6).jpg)

1.png)

_(5).jpg)

.jpg)

_(4).jpg)

_(1).jpg)

_(2).jpg)

.png)