Payroll taxes are one of the most critical responsibilities for any employer. Yet, many businesses—especially startups and expanding companies—often underestimate the complexity of managing payroll tax liabilities. From calculating statutory deductions to ensuring timely filings, payroll tax compliance requires accuracy, awareness, and efficient systems.

In today’s regulatory environment, understanding payroll tax liabilities is not just about avoiding penalties—it’s about building a financially responsible and compliant organization.

In this guide, we break down payroll tax liabilities, why they matter, and how businesses can manage them efficiently.

What Are Payroll Tax Liabilities?

Payroll tax liabilities refer to the taxes that employers are required to withhold from employees’ salaries and contribute to government authorities. These taxes are typically calculated based on wages, bonuses, commissions, and other employee compensation.

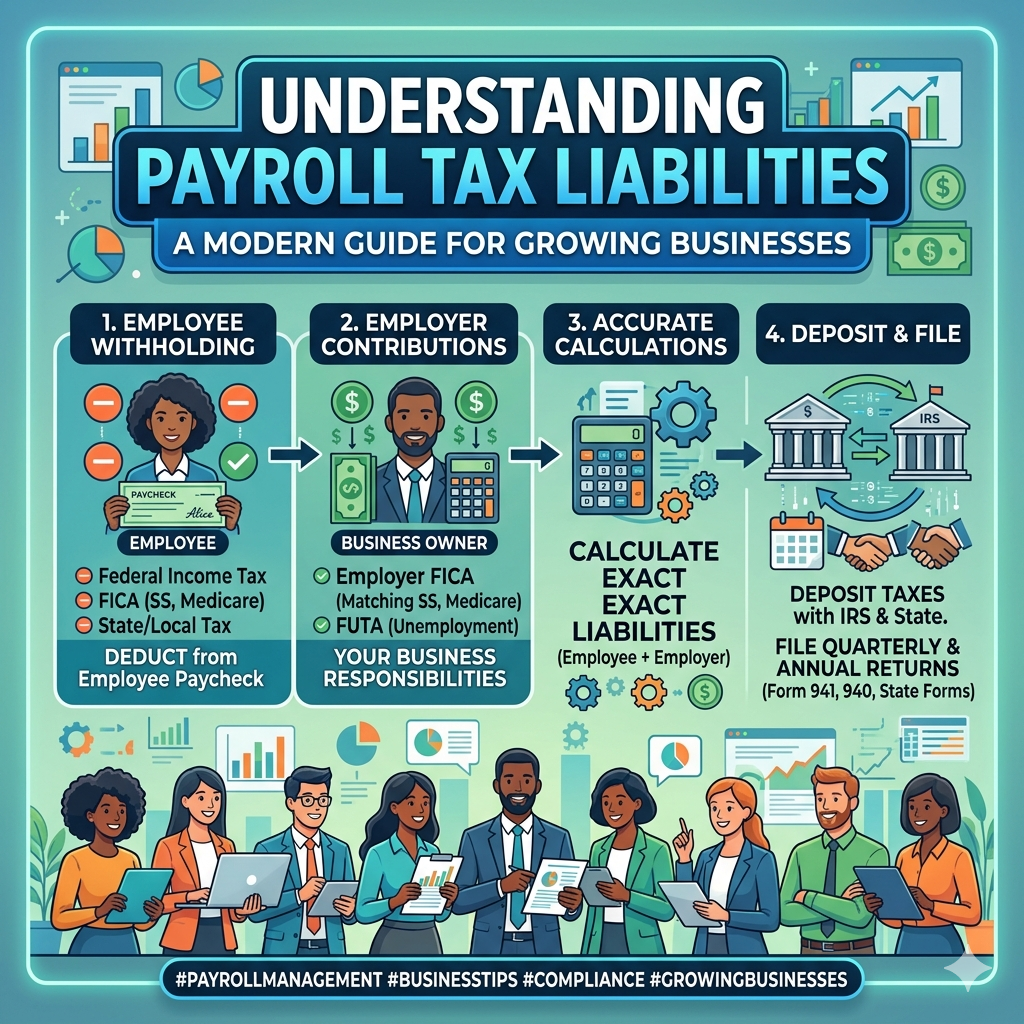

Payroll tax obligations generally fall into two categories:

1. Employee Withholdings

These are taxes deducted directly from employee salaries, including income tax and other statutory deductions.

2. Employer Contributions

Employers are also responsible for contributing certain taxes on behalf of their employees, which may include social security, insurance contributions, or other statutory funds depending on the country.

Together, these obligations form a company’s payroll tax liability.

Key Components of Payroll Tax Liabilities

Understanding the major components helps businesses remain compliant and maintain accurate financial records.

1. Income Tax Withholding

Employers must deduct applicable income tax from employee wages based on government tax slabs and submit it to the appropriate tax authorities.

2. Social Security Contributions

In many countries, employers contribute to government-managed social security programs that support pensions, disability benefits, and retirement plans.

3. Employee Insurance Contributions

Mandatory insurance programs may include health insurance, employment insurance, or workplace injury compensation.

4. Retirement Fund Contributions

Many governments require employers to contribute to retirement funds such as provident funds or pension schemes.

Each of these deductions must be calculated accurately and remitted within specified deadlines.

Why Payroll Tax Compliance Is Crucial

Ignoring payroll tax responsibilities can have serious financial and legal consequences.

Avoiding Government Penalties

Late payments or incorrect filings can lead to heavy fines, interest charges, or legal complications.

Maintaining Employee Trust

Employees rely on employers to properly manage deductions like retirement contributions and taxes. Incorrect payroll processing can damage workplace trust.

Ensuring Accurate Financial Reporting

Payroll taxes affect company financial statements, budgeting, and forecasting. Proper management ensures financial transparency.

Common Payroll Tax Challenges Businesses Face

Even experienced organizations struggle with payroll tax complexities. Some of the most common challenges include:

Frequent regulatory changes

Tax regulations and compliance requirements are updated regularly.

Manual calculation errors

Spreadsheet-based payroll systems increase the risk of mistakes.

Missed filing deadlines

Multiple tax authorities often require submissions at different intervals.

Multi-location compliance

Companies operating in multiple regions must follow different tax regulations.

These challenges often increase administrative workload and compliance risk.

Best Practices for Managing Payroll Tax Liabilities

To reduce risk and maintain smooth payroll operations, businesses should implement the following practices:

Automate payroll processes

Modern payroll software can calculate taxes, generate reports, and track liabilities automatically.

Maintain organized payroll records

Accurate documentation is essential for audits and regulatory checks.

Stay updated on tax regulations

Businesses must regularly monitor changes in payroll tax laws.

Conduct periodic payroll audits

Routine internal audits help identify discrepancies early.

Partner with payroll experts

Outsourcing payroll functions to professionals ensures accuracy and compliance.

How Payroll Outsourcing Simplifies Tax Compliance

For many companies, managing payroll taxes internally can be time-consuming and risky. Payroll outsourcing providers offer specialized expertise, automated systems, and compliance support.

By outsourcing payroll operations, businesses can:

Reduce administrative workload

Ensure timely tax filings

Minimize compliance risks

Improve payroll accuracy

Focus on strategic business growth

Payroll outsourcing is especially beneficial for companies expanding globally or operating across multiple tax jurisdictions.

Final Thoughts

Payroll tax liabilities are an unavoidable part of running a business, but they don’t have to be overwhelming. With the right systems, knowledge, and professional support, companies can manage payroll taxes efficiently while maintaining compliance with government regulations.

As businesses grow and regulations evolve, having a structured payroll strategy becomes essential for financial stability and operational success.

Organizations that invest in accurate payroll tax management not only avoid penalties but also create a stronger foundation for long-term growth.

_(6).jpg)

1.png)

_(5).jpg)

.jpg)

_(4).jpg)

_(1).jpg)

_(2).jpg)

.png)